Most coverage of Bima Sugam explains how customers may use the portal to compare and buy insurance.

That is only half the story.

Bima Sugam is also a listed-stock story. It could change who controls insurance discovery, how distributors earn money and how much investors should pay for businesses built around insurance distribution.

The direct question is simple:

What happens to PB Fintech, the parent company of Policybazaar, if even 15 to 20 percent of standard motor and retail health insurance purchases shift to a regulator-backed marketplace with no traditional distributor commission?

The answer is not that Bima Sugam will immediately effect Policybazaar or insurance company earnings. The immediate financial effect may be smaller than the headlines suggest.

The bigger risk lies in valuation.

Investors currently pay high earnings multiples for several insurance and insurance-distribution stocks because they expect years of premium growth, customer retention and profitable distribution. Bima Sugam could force the market to question how durable those assumptions are.

The premium-shift figures use FY26 motor and retail health industry premium. The PB Fintech revenue estimate uses an assumed addressable product share and an illustrative revenue yield. It is a scenario analysis, not management guidance or a forecast.

The premium-shift figures use FY26 motor and retail health industry premium. The PB Fintech revenue estimate uses an assumed addressable product share and an illustrative revenue yield. It is a scenario analysis, not management guidance or a forecast.

What Has IRDAI Confirmed About the Bima Sugam Launch?

IRDAI Chairman Ajay Seth said the first insurance products on Bima Sugam are expected to become available by the end of September 2026.

Motor insurance is expected to come first, followed by health insurance and term life insurance. The rollout will happen in phases as insurers complete their product and technology integrations.

Bima Sugam is being developed as digital public infrastructure for insurance. It will bring customers, insurers and intermediaries onto a common platform for purchasing, servicing and managing insurance policies.

It is often described as a government insurance marketplace in India. That description needs some qualification.

Is Bima Sugam Really a Zero-Commission Insurance Platform?

Bima Sugam is designed to remove the traditional distributor commission from transactions completed directly through the platform.

But zero commission does not necessarily mean zero cost.

The platform will still require technology, policy servicing, payment processing, customer support and operating infrastructure. Public reporting has indicated that nominal marketplace or transaction fees may apply, but a final universal fee schedule has not yet been published.

This distinction matters for investors.

The economic impact will depend on the difference between:

- What an insurer currently spends to acquire a customer through an agent, broker, bancassurance partner or digital aggregator

- What the insurer will pay to complete and service the same transaction through Bima Sugam

- How much of the saving the insurer retains

- How much gets passed to the customer through lower premiums

- Whether increased price competition removes the saving altogether

Also Read Bima Sugam Rollout: Is India's "UPI for Insurance" Finally Here?

Why Bima Sugam Is a Stock Market Story

Bima Sugam does not create new insurance risk. It changes the route through which insurance reaches the customer.

That makes it a distribution event.

Distribution affects three things that matter to shareholders:

- Customer acquisition cost: How much an insurer spends to sell a policy

- Pricing power: Whether the insurer can charge more for similar coverage

- Channel ownership: Whether the insurer or distributor controls the customer relationship

Policybazaar has built its business around solving these problems.

It helps customers discover products, compare policies, receive advice, complete purchases and manage renewals. Insurers pay for access to this demand and distribution infrastructure.

Bima Sugam aims to place much of the same activity on shared industry infrastructure.

That does not make Policybazaar irrelevant. It does, however, create a public alternative for some of the most standardised insurance products.

The Direct Market-Size Math

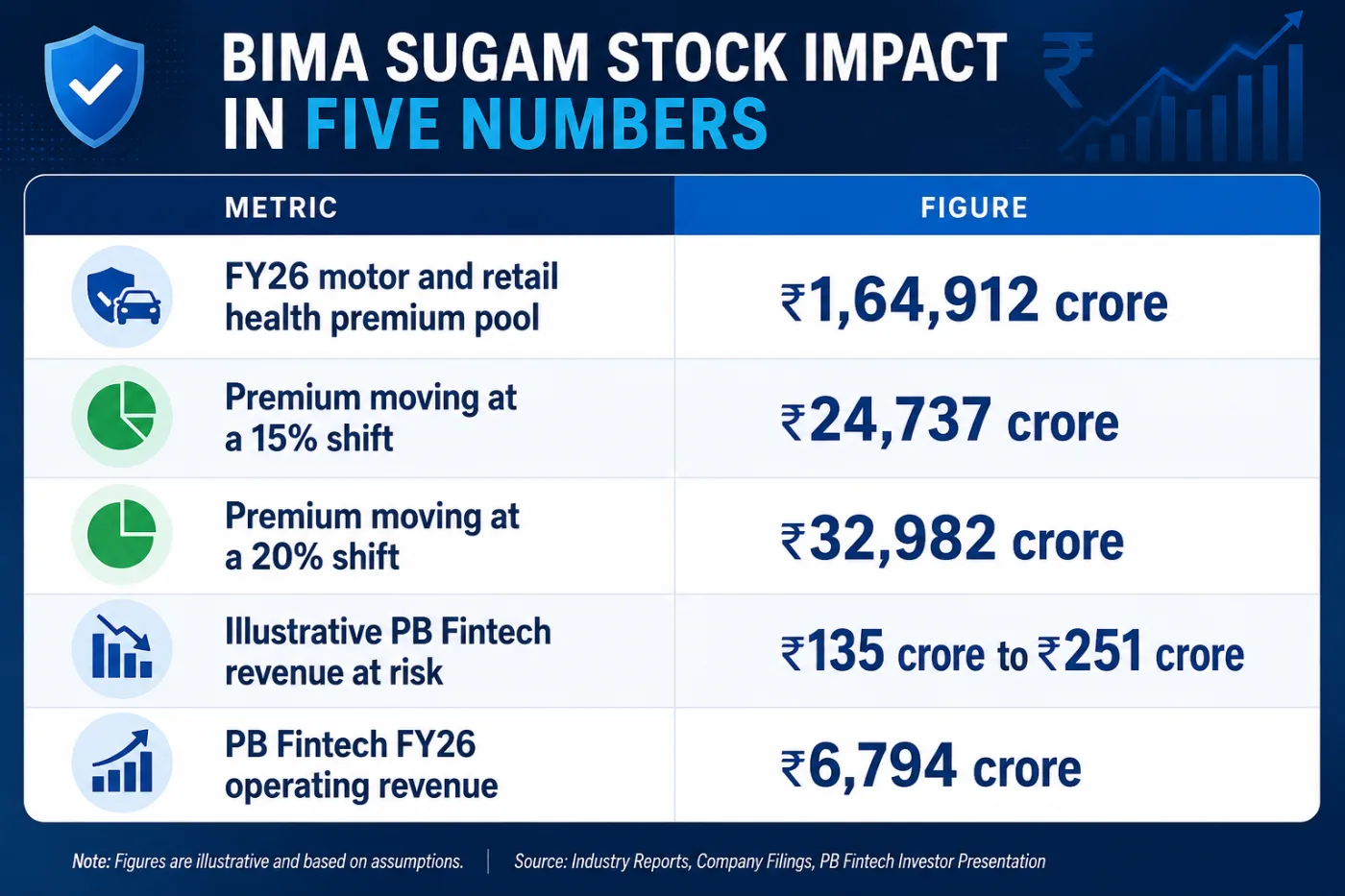

India’s non-life insurance industry collected approximately ₹3.36 lakh crore in gross direct premium during FY26, an increase of 9.3 percent.

Motor insurance contributed about ₹1.08 lakh crore. Retail health insurance contributed another ₹56,696 crore.

Together, these two categories represent an annual premium pool of approximately:

₹1,64,912 crore

This is a practical starting point for measuring the possible Bima Sugam impact because motor and retail health products form part of the initial rollout.

It is not a claim that the entire pool will immediately become available for direct online purchase. Commercial motor, complex health cases, employer policies and advice-led sales may remain dependent on intermediaries.

Also Read Insurance FDI Hits 100%: Foreign Firms Can Now Fully Own Indian Insurers

How Does Policybazaar Earn Money?

Policybazaar does not underwrite insurance or retain insurance risk. It operates as a distribution and technology platform.

Its economics come from helping insurers acquire and retain customers through:

- New policy sales

- Renewals and trail income

- Customer assistance

- Product comparison

- Call-centre and advisory support

- Claims-related assistance

- Insurer integrations

- Offline and partner-led distribution

PB Fintech reported total insurance premium of ₹29,934 crore in FY26, an increase of 42 per cent.

Its consolidated operating revenue increased 37 per cent to ₹6,794 crore, while profit after tax rose to ₹670 crore. The company had sold more than 67 million policies through March 2026.

Its insurance renewal revenue annual run rate also increased to ₹1,126 crore from ₹689 crore a year earlier.

How Will Bima Sugam Affect Policybazaar?

Bima Sugam directly overlaps with several parts of the Policybazaar customer journey.

A customer may eventually be able to:

- Compare standard insurance products

- View pricing and policy details

- Purchase directly from an insurer

- Store policies in one account

- Request servicing

- Complete renewals

- Track claims or policy-related requests

This overlap is strongest in standard motor insurance, retail health policies and simple term insurance.

These products are easier to compare than complex savings, annuity or investment-linked policies.

What Part of Policybazaar’s Moat Is Most Exposed?

Bima Sugam presents the largest challenge to Policybazaar’s role as the main digital starting point for insurance discovery.

If customers begin their search on Bima Sugam, Policybazaar could face pressure in three areas:

- Lower customer traffic: Fewer consumers may start their insurance search on Policybazaar.

- Reduced commission bargaining power: Insurers may have a lower-cost alternative for standard products.

- Higher marketing pressure: Policybazaar may have to spend more to protect its share of customer searches.

The threat is not limited to customers completing transactions on Bima Sugam.

PB Fintech Earnings Impact: A 15 to 20 Per cent Shift Model

PB Fintech does not publicly provide enough product-level data to calculate the exact share of its insurance premium coming from standard motor and retail health products.

Any direct earnings estimate must therefore use assumptions.

The following model uses:

- FY26 insurance premium handled by PB Fintech: ₹29,934 crore

- Assumed share linked to addressable motor and health products: 60 percent

- Illustrative revenue yield on affected premium: 5 to 7 percent

- Premium shift to Bima Sugam: 15 to 20 percent

The 5 to 7 percent range is a scenario assumption, not a disclosed PB Fintech take rate.

What Does Bima Sugam Mean for Insurance Stocks?

Bima Sugam will not affect every insurance company in the same way.

The outcome will depend on product mix, distribution channels, acquisition expenses, brand strength and current valuation.

LIC: Lower Valuation, Large Agency Exposure

LIC was trading at approximately 9.6 times earnings around July 14, 2026, far below most private listed life insurers.

Its low valuation may limit immediate multiple risk from Bima Sugam.

LIC also has a large agency network and a customer base that remains less dependent on online comparison platforms. This gives it distribution reach, but it also creates a cost structure that could face pressure if direct sales gain share.

LIC’s FY26 investor presentation provides useful evidence.

The insurer reported value of new business of ₹14,179 crore, an increase of 41.6 percent, with a VNB margin of 21.2 percent.

Also Read Top Insurance Companies in India by AUM, Premium & Growth in FY26

HDFC Life, SBI Life and ICICI Prudential Life

Private life insurers trade at higher valuation multiples because investors expect stronger growth, better product mix and higher future profitability.

Around July 14, 2026:

Listed Life Insurer Approximate P/E

LIC 9.6

HDFC Life 65.1

SBI Life 74.6

ICICI Prudential Life 46.1

P/E is not the best standalone measure for a life insurer. Investors also track embedded value, VNB growth, VNB margin and return on embedded value.

Still, the table shows how differently the market prices these companies.

HDFC Life reported FY26 VNB of ₹4,034 crore and a VNB margin of 24.2 percent.

SBI Life reported FY26 embedded value of ₹80,790 crore and VNB of ₹6,670 crore. Its VNB margin stood at 27.5 percent.

SBI Life’s commission ratio was 4.4 percent, while its total cost ratio was 10.6 percent. Bancassurance contributed 60 percent of annualised premium equivalent, agency contributed 29 percent and other channels contributed 11 percent.

Will Bima Sugam Reduce Insurance Premiums?

Lower commission does not guarantee lower premiums.

Insurance pricing also depends on:

- Claims costs

- Medical inflation

- Vehicle repair costs

- Fraud

- Reinsurance costs

- Underwriting expenses

- Taxes

- Operating costs

- Regulatory requirements

Insurers may pass part of the distribution saving to customers.

They may also retain the saving to improve margins, especially in products where claims ratios remain high.

Competition will determine how much reaches the policyholder.

In motor insurance, where customers can compare similar products easily, more of the saving may be passed through.

In health insurance, differences in coverage and underwriting make direct price comparison harder. Insurers may retain a larger part of the saving or use it to improve benefits.

Is Bima Sugam a UPI Moment for Insurance?

The phrase “UPI moment for insurance” is useful, but only up to a point.

UPI succeeded because it created shared payment rails with broad participation, simple customer use and low transaction friction.

A failed payment can be reversed quickly. A poorly selected health policy may affect a family several years later during a hospitalisation.

Bima Sugam can standardise infrastructure. It cannot remove the need for advice in every insurance category.

Also Read AI Insurance India Is Here — Meet jUMPP, the App That Makes Buying Policies as Easy as Chatting!

What Investors Should Track Between July and September 2026

Investors should look beyond the launch announcement and monitor actual operating data.

The most important indicators will be:

- Final platform fee: The difference between existing distribution cost and the Bima Sugam fee will determine the economic saving.

- Number of insurers live: A marketplace with limited participation will not offer meaningful comparison.

- Products available: Standard motor renewals may shift faster than new health policies requiring medical underwriting.

- Customer traffic: App downloads and registrations matter less than completed policy transactions.

- Premium completed on the platform: This will show whether Bima Sugam is becoming a real distribution channel.

- Renewal rates: The platform becomes more valuable if customers also return for renewals.

- Policybazaar marketing cost: Rising advertising expenditure could indicate stronger competition for customer traffic.

- PB Fintech insurance premium growth: A slowdown in motor or health premium growth after the launch would be an early warning.

- Insurer commission ratios: Falling commission expenses without lower margins would support the positive case for insurers.

- Pricing changes: Lower premiums would show that customers, rather than insurers, are receiving the economic benefit.

The Bottom Line

Bima Sugam is not automatically a Policybazaar killer.

PB Fintech has scale, brand recognition, customer data, renewal income, advisory capability and claims support. These assets cannot be recreated simply by launching a website.

But Bima Sugam can weaken the idea that Policybazaar must remain the default digital gateway for insurance.

A 15 to 20 per cent shift in India’s motor and retail health insurance premium would move approximately ₹24,700 crore to ₹33,000 crore through the new marketplace.

Under a central PB Fintech scenario, the gross annual revenue at risk could be around ₹135 crore to ₹251 crore. That may not cause a major earnings collapse.

The more important question is whether investors continue to value PB Fintech at more than 100 times earnings after a regulator-backed alternative begins offering direct insurance comparison and purchase.

For insurers, the impact is mixed.

Sources: IRDAI, Bima Sugam India Federation, General Insurance Council